The AI Funding Loop

If you’ve been watching the headlines around Artificial Intelligence lately, you’ve probably noticed a familiar pattern: the same handful of companies keep showing up, and the dollar amounts keep getting bigger. What’s far less noticeable, unless you look under the surface, is just how circular the money flows have become. Capital is moving in tight loops between a small group of companies, where one firm invests in another, which then spends that money back with the original investor, creating a closed ecosystem of funding, infrastructure, and valuation growth. And because these companies now make up a meaningful share of the stock market’s returns, this matters for investors more than ever.

Take OpenAI, the company behind ChatGPT. In 2019, when the company was still relatively unknown, it was valued at approximately $1 billion. Today, its private valuation is closer to $500 billion, roughly the size of JPMorgan or Walmart. That kind of growth doesn’t happen on hype alone. This is because large players, such as Microsoft, SoftBank, Oracle, Nvidia, and others, are investing tens of billions of dollars in building the infrastructure necessary to power AI.

Microsoft was the first major backer, investing $1 billion in 2019 and then an additional $10 billion in 2023. That stake is now worth around $135 billion, a 27% ownership position in a company that didn’t even exist in the public consciousness a few years ago. But here’s where the loop begins: OpenAI doesn’t just take Microsoft’s investment and put it in the bank. It turns around and spends billions on Microsoft’s Azure cloud services. Microsoft funds OpenAI, which in turn pays Microsoft, resulting in Microsoft reporting higher revenue and utilizing its financial strength to continue funding OpenAI. It’s a mutually reinforcing cycle.

And Microsoft isn’t the only one in the loop. Earlier this year, OpenAI raised another funding round, “up to” $40 billion, led by SoftBank, a global investment firm best known for backing Uber and other high-growth tech companies. That money is helping launch something called “Project Stargate,” a $500 billion plan to build out new data centers across the U.S. over the next four years. The project brings together OpenAI, Oracle, and SoftBank to scale the amount of computing power needed for AI to keep growing. Oracle isn’t just helping build the project; it’s also signed a deal for OpenAI to buy $300 billion of cloud computing capacity over five years. To make that possible, Oracle announced that it would purchase $40 billion of Nvidia chips, the hardware that actually enables large-scale AI models to run.

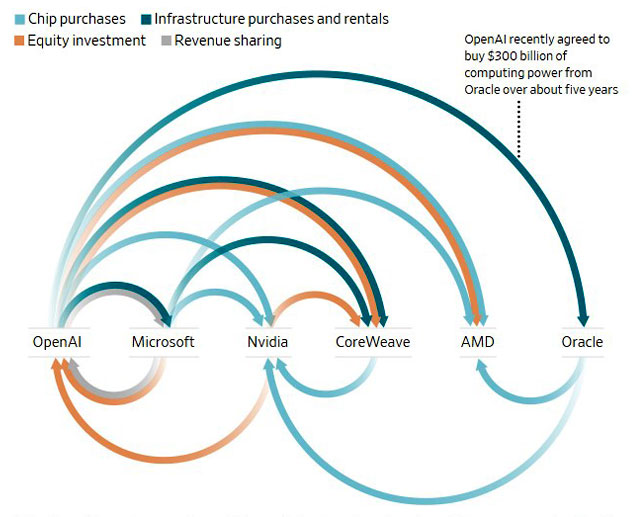

Select capital flows among six Al-industry companies

Source: WSJ

Here’s what that loop (illustration above) looks like below, in simplified form.

At the hardware level, Nvidia isn’t just selling chips; it also owns part of CoreWeave, a fast-growing cloud provider whose entire business runs on Nvidia’s technology. CoreWeave currently has more than $15 billion in infrastructure contracts with OpenAI, and OpenAI’s demand helps fund additional Nvidia chip orders, which in turn increase Nvidia’s revenue and support its stock price, allowing Nvidia to invest back into companies like CoreWeave. The cycle continues.

Even AMD (Advanced Micro Devices), Nvidia’s biggest competitor, has joined the mix. This fall, it signed a multi-year deal to supply chips to OpenAI, with an option for OpenAI to buy up to 10% of AMD. Similar to the Microsoft-OpenAI structure, as OpenAI expands, it will require more chips, creating both revenue and valuation upside for AMD.

If this feels like a lot of money circulating among the same few firms, that’s precisely the point. The AI “boom” hasn’t spread widely across the market. It’s heavily concentrated in companies that both fund and supply each other. A closed loop that amplifies valuations on the way up.

So what does all this mean for investors?

First, it helps explain why a relatively small number of companies have been responsible for the majority of stock market returns over the past year. When capital, earnings, and investment momentum are all flowing through the same channels, the impact on share prices is magnified. Companies inside the loop grow faster, receive more attention, and attract more investment, sometimes before the underlying business fundamentals have fully caught up.

Second, it highlights both the opportunity and the risk of concentration. There is no doubt that AI is reshaping industries and creating a genuine demand for computing power, data centers, and advanced chips. But when growth becomes circular, when companies are both each other’s customers and funders, it can also create feedback loops that unwind quickly if expectations change. We’ve seen this before in other cycles: the dot-com era, the telecom buildout of the early 2000s, and even the clean-tech surge in the late 2000s. Innovation is real, but market enthusiasm often outpaces it.

Third, it serves as a reminder that long-term investing still benefits from diversification, even when a single theme appears unstoppable. These companies may continue to grow, and AI may be one of the defining technologies of the decade. However, even the strongest secular trends undergo corrections. History almost always rewards investors who participate, not those who chase.

The takeaway isn’t to avoid AI or to assume it’s in a bubble. It’s simply to understand how much of today’s market movement is being driven by a small group of interconnected players, and to make sure your exposure reflects not just the excitement, but the potential volatility that comes with it.

Innovation can transform markets, but discipline is what protects portfolios.

~ KWB Team

The views expressed are those of the author and are subject to change. Certain statements may be forward-looking and are not guarantees of future performance. References to specific companies are for illustrative purposes only and do not constitute a recommendation. KWB Wealth is not affiliated with and does not receive compensation from the companies mentioned. Investing involves risk, including possible loss of principal.