Are We in a Bubble?

There’s been a noticeable rise in clients asking the same question lately: “Are we in a bubble?” It comes up in meetings, in emails, even in casual conversation. And it makes sense. The market has been strong, headlines continue to point to “overvaluation,” and whenever a small group of stocks leads the way, people start thinking about 1999, 2007, or whatever past crash feels most familiar. That anxiety got louder on November 4th when the Nasdaq 100 dropped over 2% in a single day, and the most common explanation wasn’t earnings or interest rates, but simply “bubble fears.”

So let’s take the question seriously, the way we would if you and I were sitting across the table from each other. Because the real concern isn’t whether the market is up, it’s whether the market is detached from reality.

A bubble isn’t just “a market that has gone up a lot.” A bubble is what happens when prices rise far faster than a business’s real-world value can justify. It’s when investors stop asking, “What is this actually worth?” and instead say, “I just don’t want to miss out.” That’s what led to tulip bulbs selling for the price of a house in the 1600s, internet companies going public with no revenue in 1999, and homes appreciating 30–40% above fundamentals in 2007. Those weren’t just strong markets; they were markets disconnected from reality.

The question today isn’t “Has the market gone up?” It’s “Has it gone up in a way that doesn’t make sense?”

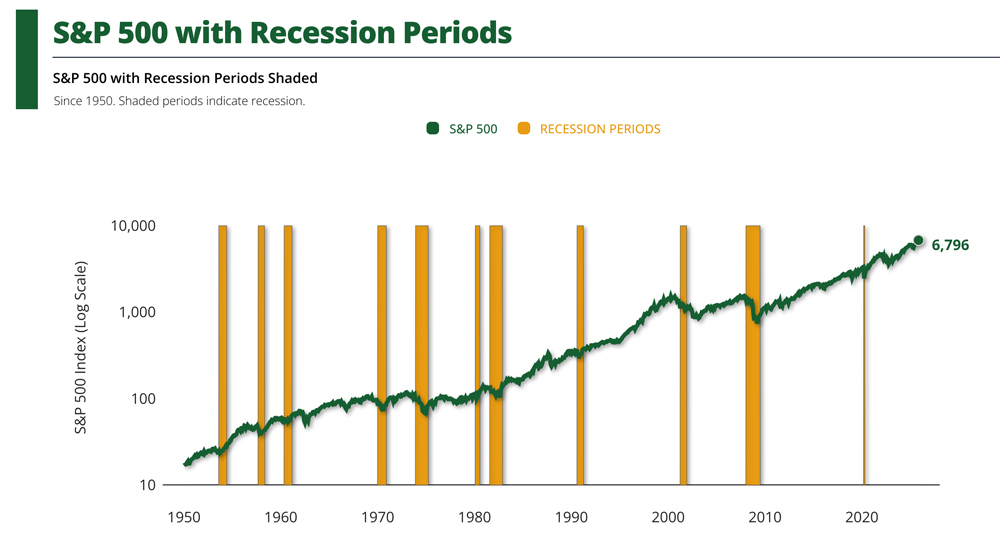

If you look at a long-term chart of the S&P 500 going back to 1950, you can clearly see the late 1990s bubble. It sticks out like a cliff. A massive surge followed by a steep drop.

Source: © Exhibit A, FactSet Research Systems Inc., Standard & Poor's, Federal Reserve Bank of St. Louis via FREDPoor's | Latest: 2025-11-05

By comparison, today’s rise looks like a continuation of the long-term upward trend, not a sudden spike. It’s elevated, yes, but it’s not vertical. That distinction matters.

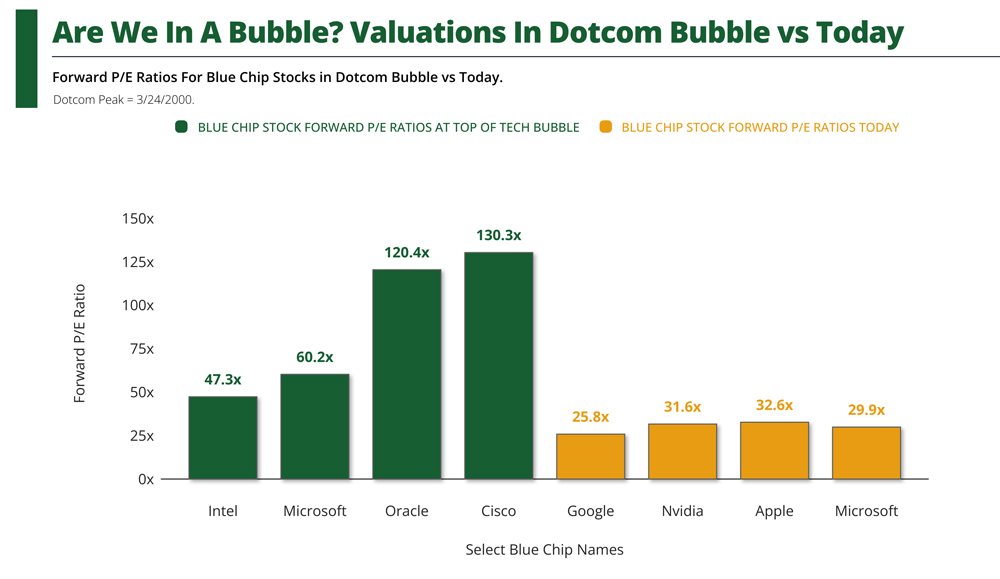

The same is true if you compare valuations today with valuations during the dot-com era.

Source: © Exhibit A, FactSet Research Systems Inc.Poor's | Latest: 2025-11-05

Back then, many of the largest companies were trading at 80–100x earnings, and some had no earnings at all. That’s not what we’re seeing today. Are valuations cheap today? No. But they’re also nowhere near the level where they’ve historically been labeled as a bubble.

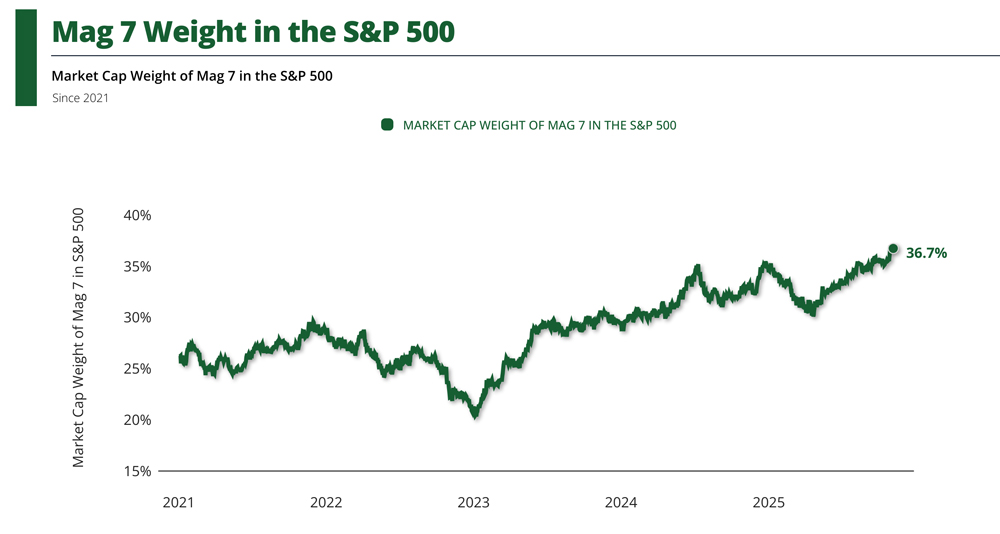

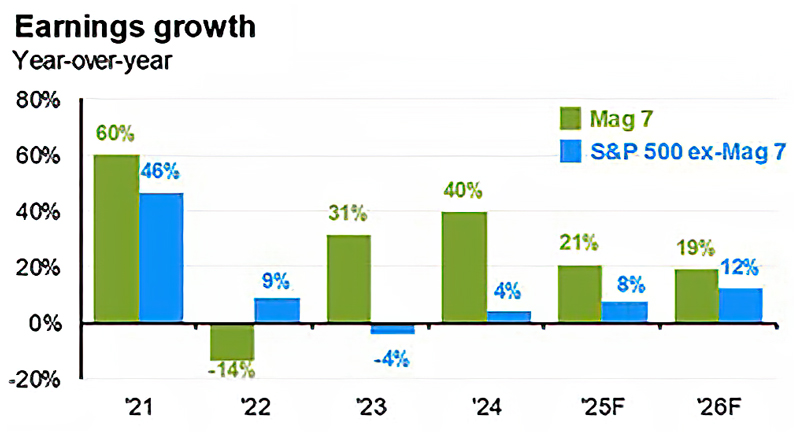

This is where the second concern usually comes in: “Okay, but isn’t the whole market just being held up by a few giant tech stocks?” The short answer is yes — but not in the way people think. In 1999, tech stocks rose because investors hoped the companies would eventually become profitable. Today, the largest companies are going up because they are already generating massive earnings, cash flow, and real-world adoption.

Source: © Exhibit A, FactSet Research Systems Inc., Standard & Poor's | Latest: 2025-11-05

Source: J.P. Morgan Asset Management, Guide to the Markets, as of 9/30/2025

Their stock prices haven’t disconnected from fundamentals; they’ve moved in line with them.

That doesn’t mean those companies will rise forever. It just means the current leadership is based on math, not mania.

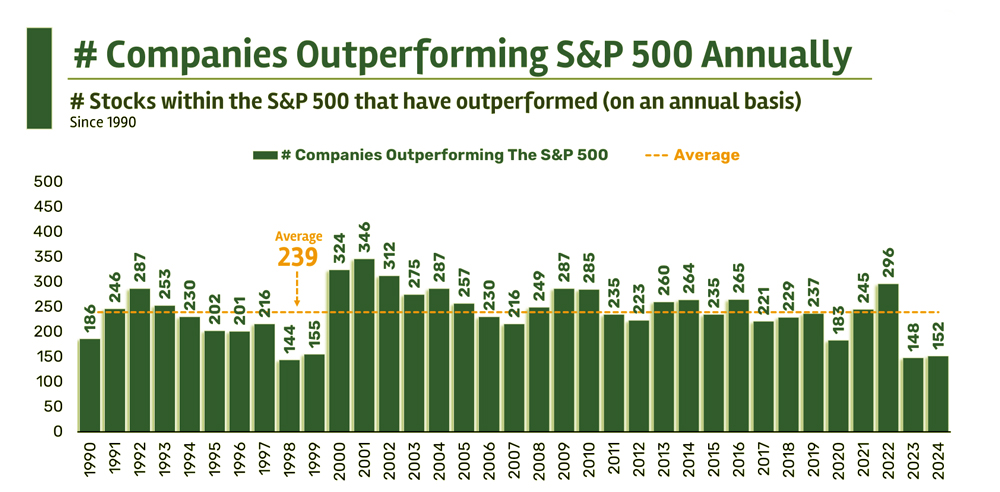

There’s also a misconception that a healthy market requires a large number of companies to beat the index. Historically, that’s not true. Since 1990, only about 239 companies in the S&P 500 beat the index in the average year, well under half.

Source: Ritholtz, data via Bloomberg Finance L.P.

In fact, the years when more companies outperform the index are almost always years when the market is down. That happened in 2000, 2001, 2002, 2008, and again in 2022. So, having a narrow group of stocks leading the market isn’t a new warning sign; it’s been a feature of most bull markets for decades.

Are we in a bubble today? Based on history, earnings, valuations, and market behavior, the answer is no. Could things evolve into a bubble if prices continue to rise without underlying earnings growth? Sure. If investors start buying simply because “everything goes up,” then we’ll have a different conversation. However, we’re not there today.

That doesn’t mean we ignore the risk. It means we handle it the same way we always do, by rebalancing when positions move too far above target, trimming areas that have run too hot, keeping portfolios diversified even when a few names dominate headlines, and staying willing to be contrarian if the data calls for it. We don’t build portfolios for the news cycle. We build them with the long-term plan in mind.

If reading this raises questions about your allocation, risk exposure, or the extent of “bubble risk” you actually have, please reach out. That’s what we’re here for, and these are the conversations that matter most before the headlines change your emotions. Your plan should always feel more solid than whatever the market is discussing that week. And if it doesn’t, let’s make sure it does.

~ Steve Gormley

This commentary reflects the personal opinions, viewpoints, and analyses of the author and should not be regarded as a description of advisory services provided by KWB Wealth. Forward-looking statements are not guarantees of future performance and involve risks and uncertainties. Actual results may differ materially from those expressed or implied.

All investing involves risk, including the potential loss of principal. No investment strategy can guarantee success or protect against loss in periods of declining values.

The S&P 500 Index and Nasdaq 100 Index are unmanaged indices and cannot be invested in directly. Index performance does not reflect the deduction of any fees or expenses.

Information contained herein is based on sources believed to be reliable; however, KWB Wealth makes no representation or warranty as to the accuracy or completeness of the information.

This material is for general informational purposes only and is not intended to provide, and should not be construed as, individualized investment, tax, or legal advice.

References to specific companies are for illustrative purposes only and do not constitute a recommendation to buy, sell, or hold any security.