The stock market is climbing and reaching new all-time highs. While this can be exciting, it raises an important question: “If the market is already at a peak, am I setting myself up for a loss if I invest now?”

It’s natural to feel cautious. After all, no one wants to buy at the top. But history, data, and financial planning experience suggest a more reassuring perspective: all-time highs are not red flags but milestones on a market’s long-term upward journey.

Let’s unpack why that’s the case, what risks to consider, and how you can confidently approach investing even when the headlines are filled with “record markets.”

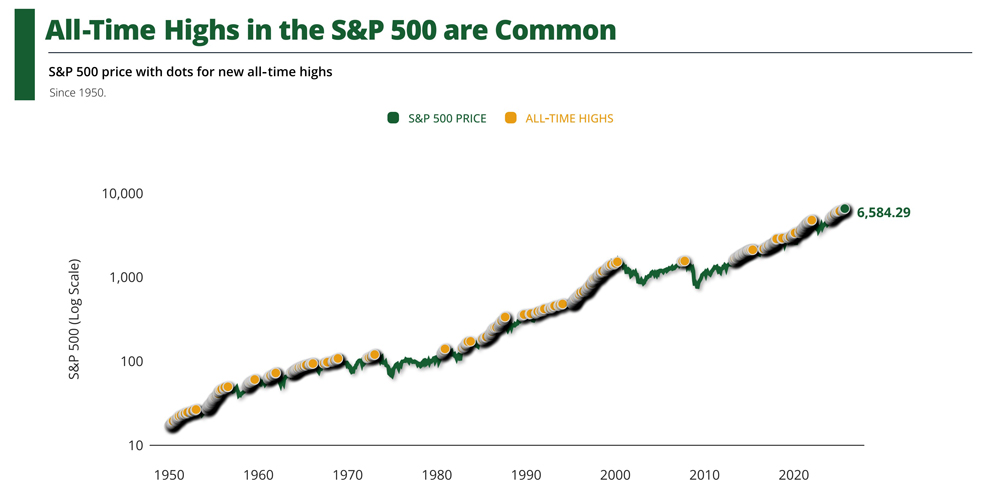

It may surprise you to learn that all-time highs are common. Since 1950, the S&P 500 has hit thousands of new highs. Looking at Chart 1, you’ll see so many new all-time highs that the dots that signify those highs run together. That’s because over the long run, businesses grow, economies expand, and corporate profits increase. As companies earn more and reinvest in themselves, their values rise, and the stock market reflects that.

Think of it this way: if markets never reached new highs, it would mean the economy had stopped progressing altogether. New highs are not unusual.

CHART ONE: Source: © Exhibit A, FactSet Research Systems Inc., Standard & Poor’s | Latest: 2025-09-14

They’re a natural and expected part of long-term investing. At every one of those highs, some investors thought, “This must be the top.” But those who stayed the course benefited from decades of growth.

When markets “feel” expensive, many people will hold off and “wait for a pullback” before investing their money. The problem with this approach is that corrections are unpredictable, and you may wait far longer than expected.

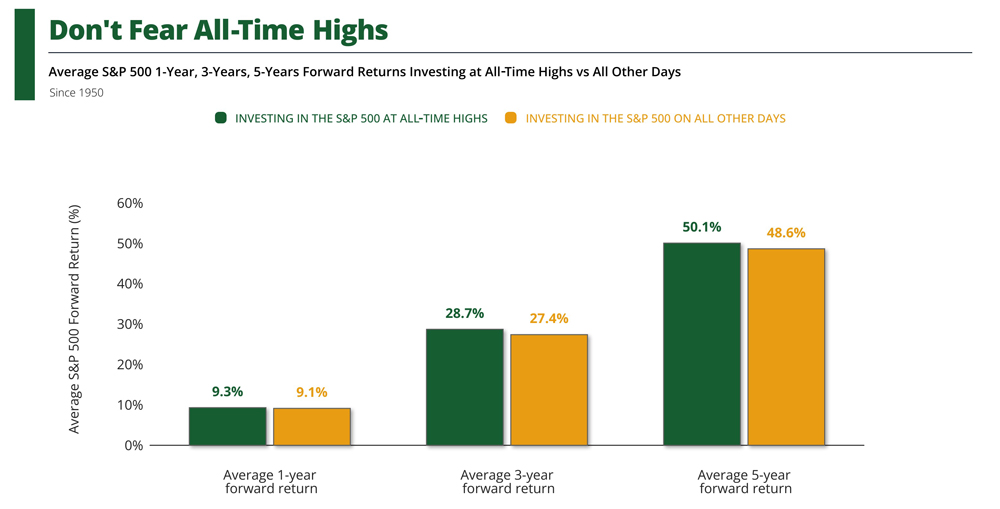

Historically, some of the most substantial returns occurred right after new highs. Chart 2 shows that shorter-term returns are actually BETTER when investing at all-time highs than investing on all other non-all-time high days.

CHART TWO: Source: © Exhibit A, FactSet Research Systems Inc., Standard & Poor’s | Latest: 2025-09-14

Therefore, if you step out or hesitate to step in, you risk missing the growth that could help you reach your goals.

There’s also the issue of inflation. Money parked in cash earns little (sometimes less than inflation), and its purchasing power erodes over time. Waiting on the sidelines might feel safe, but it quietly costs you in real terms.

Now, just because investing at all-time highs isn’t inherently risky doesn’t mean you should ignore risk altogether. The key is to align your investments with your time horizon and risk tolerance. Here are three practical strategies for investing at all-time highs, depending on your risk tolerance. First, you could use Dollar Cost Averaging (DCA). If you’re worried about putting a large lump sum into the market all at once, DCA can help. This approach involves investing smaller amounts regularly: monthly, quarterly, etc. By spreading out your purchases, you reduce the chance of putting all your money in right before a dip. Over time, this smooths out the price you pay for investments and takes emotion out of the decision.

The second strategy is diversification. No one can predict which asset class will lead in a given year. That’s why a diversified portfolio including U.S. stocks, international equities, bonds, and alternatives helps manage risk. When one part of the market struggles, another may hold up or even thrive. Diversification ensures your financial future isn’t tied to the fate of any single factor.

The last technique is incorporating a rebalancing discipline. As markets rise, your portfolio may shift to have a heavier tilt toward stocks than initially intended. Rebalancing, or periodically trimming back gains in stocks and reallocating them to bonds or cash, helps keep your risk level consistent. This forces you to “sell high and buy low” in a disciplined way.

When considering investing at highs, the most crucial factor is your timeline. Funds for short-term goals (1–3 years), like for a house purchase or tuition, should not be invested in stocks, regardless of whether markets are at highs or lows. Short-term volatility could jeopardize those goals. For medium-term goals (3–7 years), a balanced portfolio of stocks and bonds may make sense. The stock portion can grow, while the bond portion provides stability. Lastly, long-term funds (10+ years) mean market highs matter far less if your money is earmarked for retirement or legacy planning. Over long stretches, what counts most is staying invested and letting compounding do its work.

Investing is as much about behavior as it is about numbers. All-time highs can trigger fear of loss, which behavioral finance calls loss aversion. We feel losses more viscerally than gains. This emotional response can push us to act against our best interests, selling too soon or avoiding investing altogether. The antidote is having a plan. Know your allocation; stick to your rebalancing rules; focus on your goals, not the headlines. Markets will always fluctuate, but having a roadmap makes it easier to weather short-term anxiety.

So, should you invest at all-time highs? Yes, if your horizon is long and your portfolio is appropriately diversified. Yes, if you use strategies like dollar-cost averaging and rebalancing to manage risk. Yes, if you remember that records are a sign of progress, not danger. The most significant risk is not that markets will reach new highs; it’s that fear will keep you from participating in their long-term growth.

Every investor’s situation is unique. Your time horizon, risk tolerance, and goals deserve a strategy tailored to you. If you’re uncertain about investing at current levels or simply want reassurance that your portfolio is on track, talk to a KWB Wealth Manager.

At KWB Wealth, our advisors are here to help you put today’s headlines in perspective and create a plan that supports your brighter financial future with confidence.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

KWB Wealth is an SEC registered investment adviser. This material is solely for informational purposes. Advisory services are only offered to clients or prospective clients where KWB and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by KWB unless a client service agreement is in place. All investing involves risk, including the potential loss of principal, and no strategy can guarantee success. This material is for general informational purposes only and is not intended as individualized investment, tax, or legal advice.

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

No strategy assures success or protects against loss. The economic forecasts set forth in this newsletter may not develop as predicted, and there can be no guarantee that strategies promoted will be successful. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

The economic forecasts set forth in this newsletter may not develop as predicted, and there can be no guarantee that strategies promoted will be successful.