What the Private Credit Headlines Actually Mean for You

You've probably seen the headlines lately. Words like "redemption requests" and "liquidity concerns" showing up alongside private credit funds. It's the kind of language that can make anyone's stomach drop, even if you're not entirely sure what it means. So let's break it down, what's happening, why it matters, and what it means for your portfolio.

Private credit is lending outside of traditional banks. Instead of a company walking into a bank to borrow money, they borrow directly from investment funds, which provide capital in exchange for higher interest payments. Over the past decade, tighter regulations made traditional loans slower to approve, and banks became increasingly selective about which ones they'd take on at all. Companies sought alternative sources of financing, while investors were drawn to the promise of higher yields. Private credit offered both, making it a win-win. However, the environment has shifted.

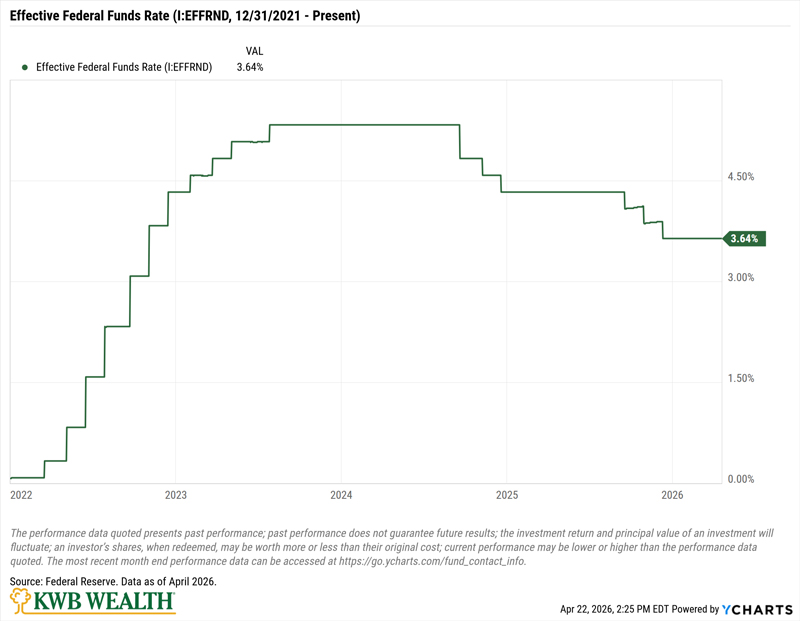

Starting in 2022, the Federal Reserve launched one of the fastest and steepest rate increases most people had ever seen, following two years of near-zero rates. As borrowing costs climbed across the economy, companies that had taken on debt began to feel the squeeze. The cash flows they once relied on to comfortably make their loan payments came under pressure. The effects weren't immediate, but as loans matured and refinancing came due at higher rates, the pressure became impossible to ignore. What had been a smooth road had developed some serious bumps.

At the same time, some private credit funds began to see a wave of investors asking for their money back. Why the sudden rush to redeem? A few things came together at once. Higher interest rates mean investors can get higher risk-free rates elsewhere, and concerns about rising defaults and financial stress among borrowers created a wave of cautiousness. Here's where the structure of these funds matters. Unlike stocks or bonds, which trade daily on public markets, private credit loans aren't easily bought or sold. When too many investors head for the exit at once, it's a little like an entire movie theater trying to leave through a single door. The funds simply aren't designed for that kind of rush.

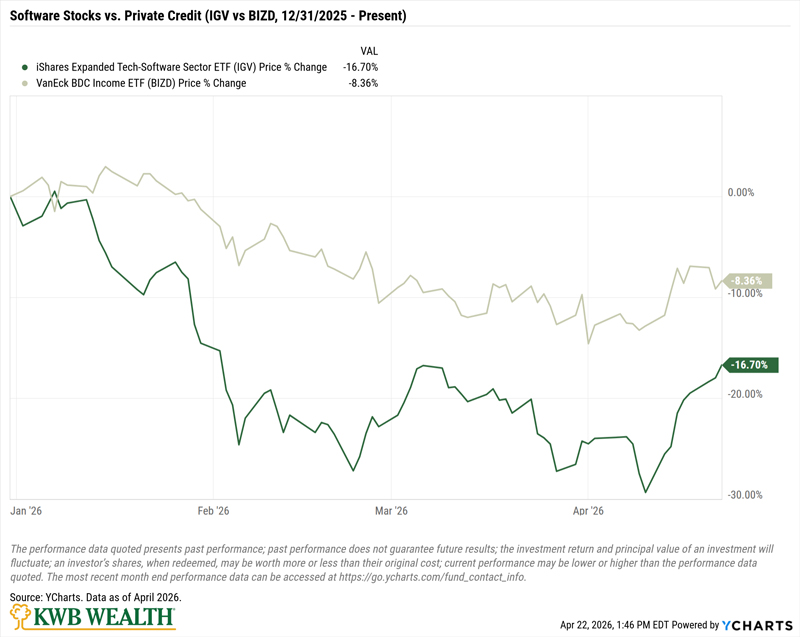

There's another layer worth understanding. A meaningful portion of private credit, roughly 21% of direct loans, has been deployed into software companies. On the surface, that made sense. Software businesses tend to have recurring revenue and predictable cash flows, which makes them attractive to lenders. But public software stocks have struggled recently as investors begin to question growth prospects and valuations. And here's the important connection: when equity markets start questioning a company's value, credit markets tend to follow. Lenders reassess risk. Capital becomes more selective. And for some funds, that shift in confidence has triggered a wave of redemption requests as investors reconsider their positions.

It's worth noting that this does not mean that all private credit or all software companies are in distress. Many businesses continue to perform well. What we're witnessing is a repricing, a recalibration driven by higher borrowing costs, more selective capital, and a sharper focus on fundamentals. That's not a collapse, but it is a meaningful shift.

KWB Wealth’s model portfolios do not include private credit vehicles at this time. We've remained committed to investments that offer daily liquidity and transparent pricing. That means you can see exactly what you own, what it's worth, and access it when you need to.

Moments like this serve as an important reminder of how different investment vehicles behave below the surface. Private credit has often been marketed as a way to earn higher yields with lower volatility. But much of that perceived smoothness comes from one simple fact: these investments aren't priced very often. Less frequent pricing can make a portfolio feel steadier than it really is. It doesn't eliminate the bumps. It just delays when you see them.

When liquidity is tested, the true nature of an investment reveals itself. It also raises a fair question: by the time strategies like this become widely available to individual investors, how much of the return opportunity has already been captured by institutional investors who got in earlier? Private credit isn't inherently bad. It continues to evolve and plays a role in the broader financial system. But in our current view, it's best suited for a narrow subset of investors, those who can genuinely afford to lock up their capital for years and remain patient when markets become constrained.

If you've seen these headlines and wondered whether any of this affects you, or if you're simply curious about how private credit fits, or doesn't fit, within a sound financial plan, we're always happy to talk it through. That's what we're here for.

~ Ricardo Salinas

Source: J.P. Morgan Asset Management, Guide to Alternatives: Private Credit, March 2025.

Private credit investments involve unique risks, including illiquidity, lack of transparency, and potential valuation uncertainty. These investments are not suitable for all investors.

Investments offering daily liquidity may experience greater short-term price volatility than less frequently valued investments.

Higher yields are generally associated with higher risk, and past characteristics of an asset class may not persist.

This commentary reflects current market conditions and is subject to change. There is no guarantee that these trends will continue.