The Third Leg: Beyond Stocks and Bonds

Most experienced investors remember 2022 as a year when nothing seemed to work. Stocks were down. Bonds were as well. Statements kept looking worse. This raised an important question: Is the traditional 60/40 portfolio still suited for today’s market?

What Changed

The foundation of the 60/40 portfolio was built on one key assumption: when stocks go down, bonds go up—and vice versa. In 2022, that relationship broke down. As interest rates climbed sharply after years of near-zero rates, bonds fell alongside stocks. The brakes failed when they were needed most. Investors expected their bond allocation to cushion the blow, but instead it added to the pain. It served as a reminder that markets evolve—and even time-tested strategies can struggle at times.

Introducing the Third Leg

Imagine a stool with only two legs. It would wobble, teeter, and fail when you need it most. This is where the third leg comes in: alternative investments. Alternatives are asset classes that exist outside the traditional mix of stocks and bonds—such as real estate, private credit, commodities, or managed futures. You may have seen last month’s blog, “What the Private Credit Headlines Actually Mean for You,” and wondered if that’s what falls into this category. Private credit is just one piece of a much broader toolkit. What makes them valuable isn’t just returns, but how they behave. Here at KWB, we focus on alternatives that offer daily liquidity and transparent pricing. Like a shock absorber on a busy road, alternatives may move more independently from stocks and bonds, which can help smooth overall portfolio volatility when the others struggle. They aren't meant to replace a traditional portfolio, but to support it, adding a third point of contact that can help keep the structure more balanced.

What the Data Is Telling Us

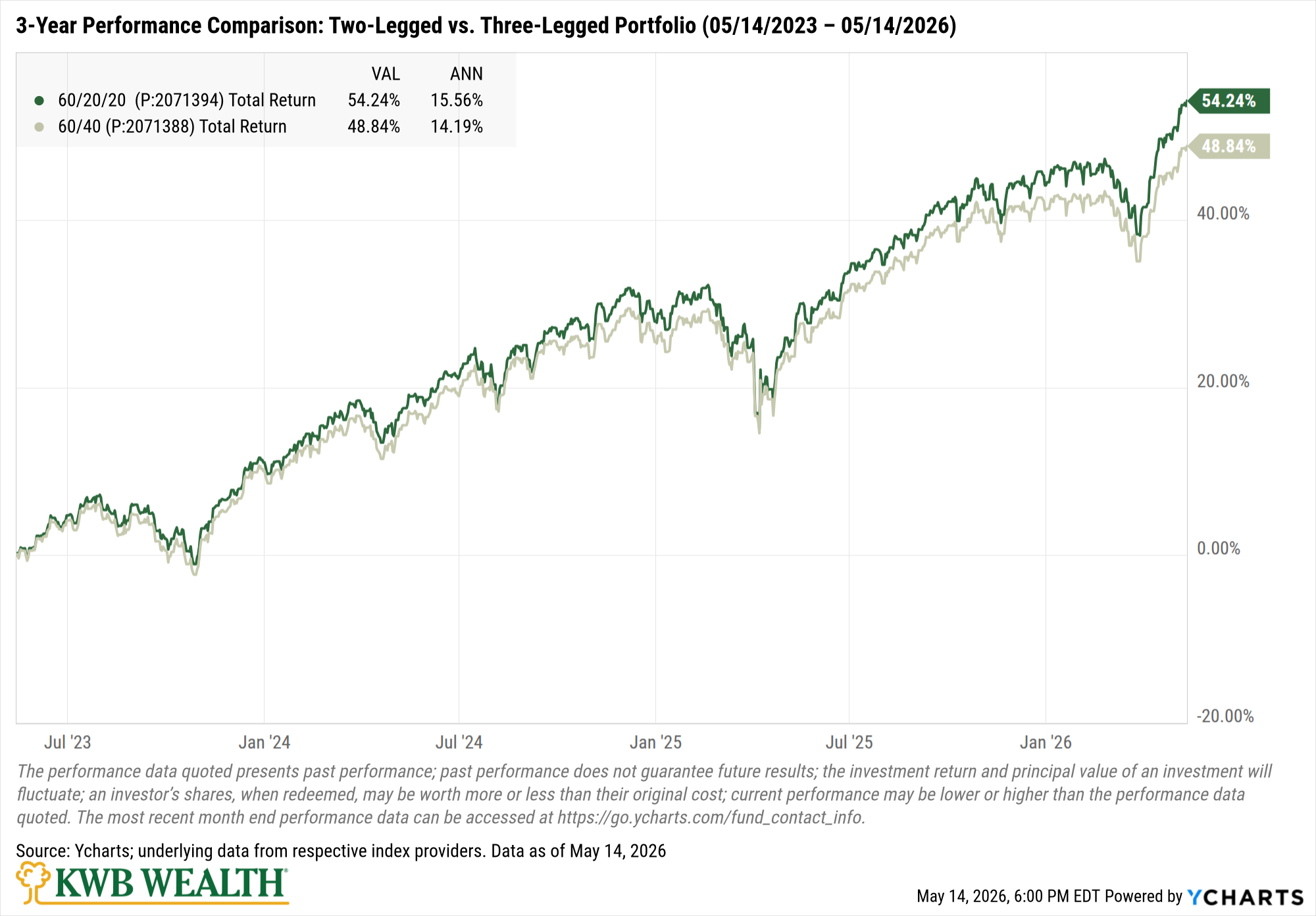

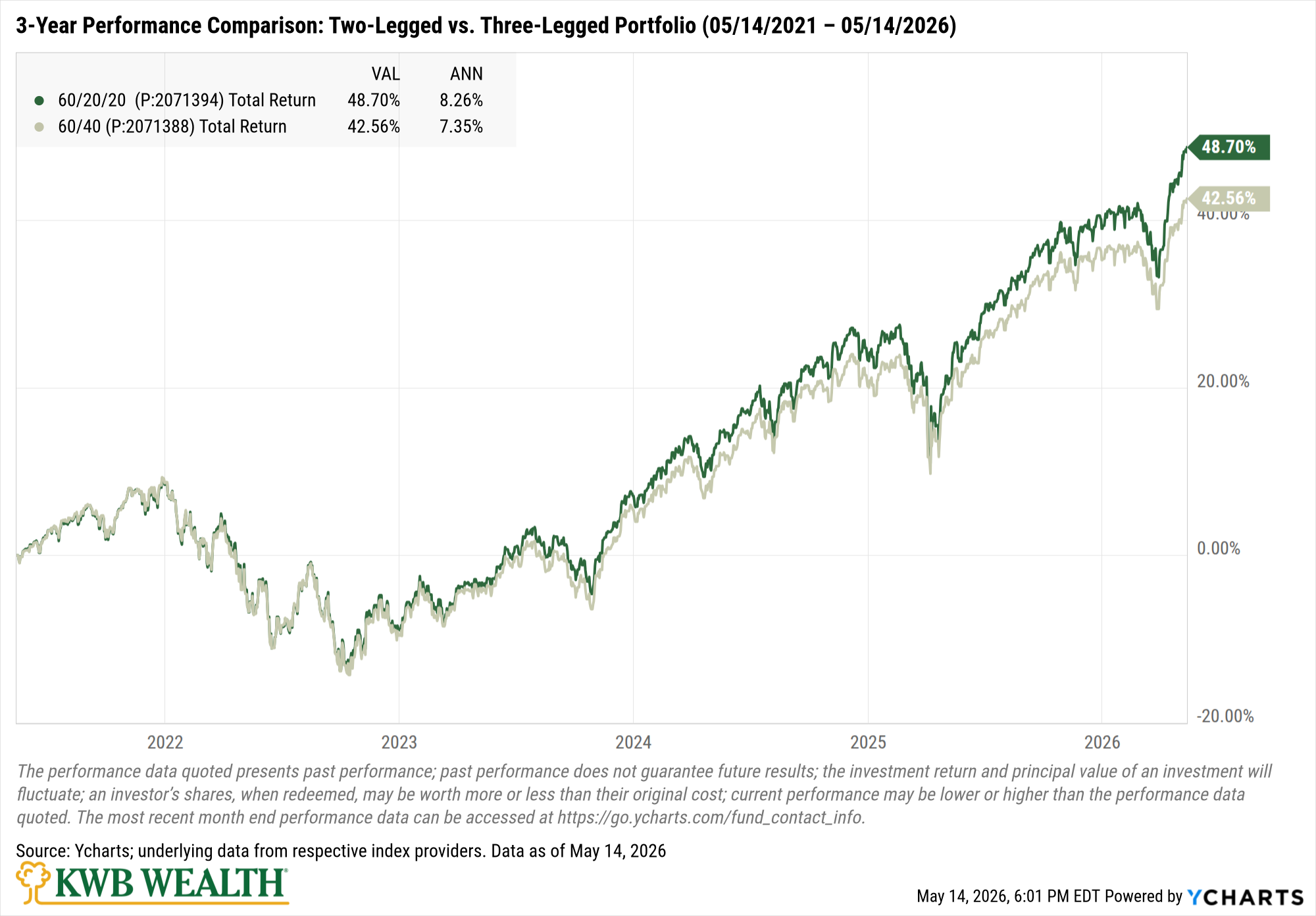

The charts below compare how two-legged and three-legged portfolios have performed over three- and five-year time frames. Together, they tell a consistent story.

- Looking at the charts above, we can see that in strong markets, the two portfolios tend to behave very similarly. Stocks are doing most of the heavy lifting.

- During periods of stress, such as 2022, the three-legged portfolio has historically helped cushion declines relative to a traditional allocation.

- The smoother overall ride of this portfolio can make it easier to stay the course in challenging times.

Why This Matters More Near Retirement

There’s a meaningful difference between a bad year at 65 and a bad year at 35. At 35, you have plenty of time to let the market rebound. At 65, you may already be taking income from your portfolio. Let’s think about what happens when the market falls while you’re taking income. Without the third sleeve, you’re having to sell stocks or bonds when they’re already down. Ultimately, locking in losses just to cover living expenses. This can have an exponentially negative effect on portfolio performance.

This is a hypothetical illustration for informational purposes only and does not represent actual investment results.

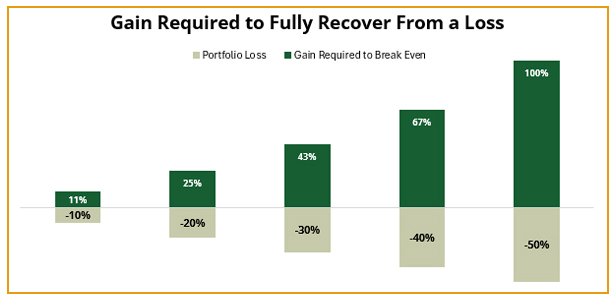

This is the perfect situation in which the third leg makes its keep. When stocks and bonds are struggling, the third leg serves as a diversifying sleeve that may behave differently from traditional assets to pull income from. Being able to pull income from something that is working and letting those who are down have time to recover can help support the portfolio’s compounding over time. This is because smaller drawdowns can lead to better long-term outcomes. Referring to the chart above, we can see that a portfolio that loses 10% only needs to gain 11% to get back to its starting point. Compared to a portfolio that loses 20%, it needs to gain 25% to get back to its starting point. The portfolio that loses less has a much smaller climb back to even, which means your money is working for you sooner. For investors taking income in retirement, this third leg can add stability that may help a retiree feel more confident. If you’ve looked at your portfolio recently, wondering if your current mix is still right for you, feel free to reach out. Portfolio construction isn’t a one-time decision. It is always worth revisiting to see what your current allocation looks like and if the three-legged approach makes sense for your financial plan. Reach out anytime.

~ Ricardo Salinas

The portfolios illustrated above are hypothetical model portfolios constructed for illustrative purposes only and do not represent actual client accounts or the results of actual trading. This is a hypothetical example and is not representative of any specific investment. Your results will vary. The 60/40 portfolio consists of 60% SPDR S&P 500 ETF Trust (SPY) and 40% iShares Core International Aggregate Bond ETF (IAGG). The 60/20/20 portfolio consists of 60% SPY, 20% IAGG, and 20% HFRI Fund Weighted Composite Index.

Past performance is not indicative of future results. Hypothetical performance results have inherent limitations and do not reflect the deduction of advisory fees, brokerage commissions, or other expenses, which would reduce returns. Actual client results will vary. Investing involves risk, including the possible loss of principal. The HFRI Fund Weighted Composite Index is unmanaged, does not reflect fees or expenses, and is not available for direct investment.

Index returns do not reflect fees or expenses. This material is intended for informational purposes only and should not be construed as investment advice or a recommendation to buy or sell any security.