Is Global Diversification Making a Comeback?

Over the past several years, a common question we heard from clients was, “Why do we own international and emerging market stocks?”

This past year, that question has shifted to something completely different: “Why don’t we have more exposure to them?”

That change isn’t random, and it doesn’t mean your portfolio was “wrong” before. It reflects something we’ve emphasized for a long time: diversification doesn’t always work, but it does over time.

For much of the past decade, U.S. markets have led the way. Given the strength of the U.S. economy, its role as the world’s reserve currency, and its technological leadership, U.S. favoritism made perfect sense and was rewarded. This year, however, global markets have responded more quickly to changing conditions, driven by policy shifts and changing investor behavior.

In our “Don’t Forget About International Stocks” blog post back in April, we highlighted developments in countries such as China and Germany that were beginning to show support for international markets. As the year progressed, those trends not only continued but strengthened, and they remain an essential part of the global investment landscape as we move into 2026.

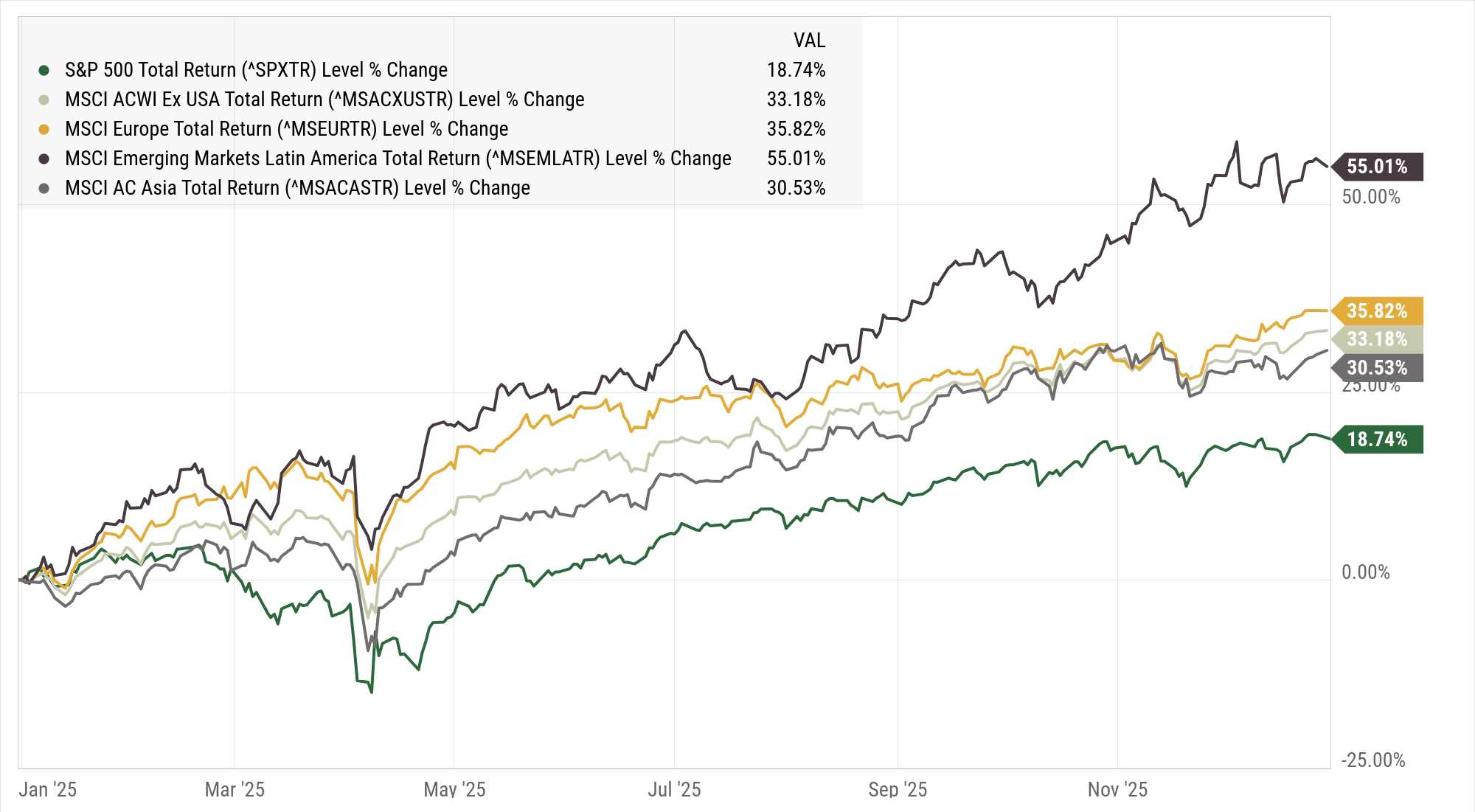

To put recent performance into context, it is helpful to examine markets across multiple time horizons. The charts below compare year-to-date returns with performance over the trailing five years.

Source: S&P Dow Jones Indices and MSCI, total return indices, via YCharts. Data reflects calendar-year performance from 1/1/2025 through 12/30/2025. Total return indices include reinvested dividends. Indices are unmanaged and cannot be invested into directly.

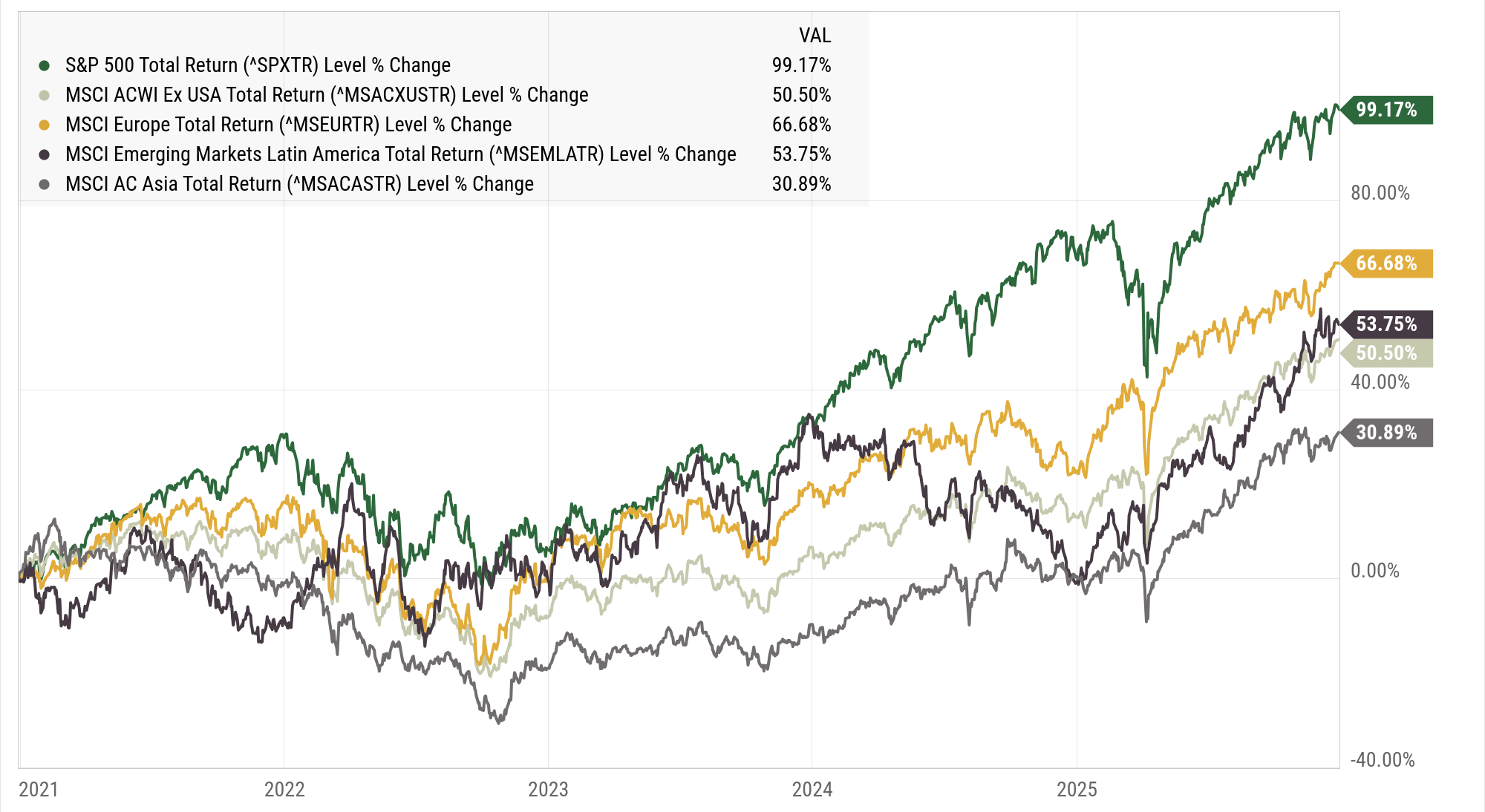

While international stocks clearly outperformed U.S. markets in 2025, a single year doesn’t define a long-term trend. That is why it’s crucial to examine the trailing five-year chart.

Source: S&P Dow Jones Indices and MSCI, total return indices, via YCharts. Data reflects cumulative performance from 1/1/2021 through 12/30/2025. Total return indices include reinvested dividends. Indices are unmanaged and cannot be invested into directly.

Market leadership tends to shift over time, often slowly, rather than all at once. These charts can help explain what has happened, but they offer little insight into what comes next. That’s why we focus less on short-term results and more on the forces driving them.

To achieve this, it’s helpful to look beyond price performance.

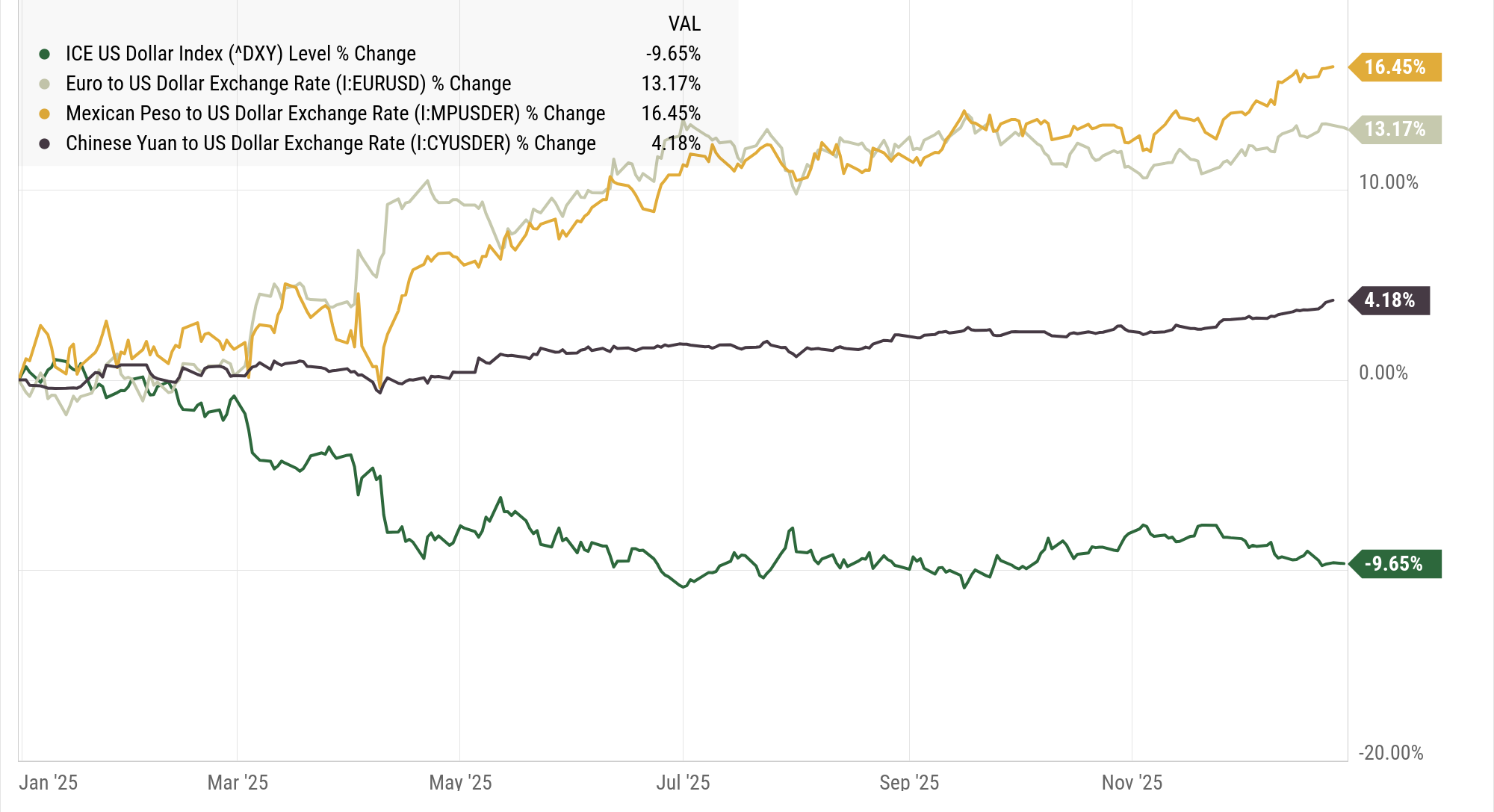

One of the most significant contributors to international market performance this year has been currency movement. Because international investments are priced in local currencies, currency movements can significantly impact returns for U.S. investors. For example, imagine exchanging $100 for euros to buy European stocks. When you are ready to sell the investment, the dollar has depreciated relative to the euro, meaning the same amount of euros now converts to $110. In this case, the additional return comes solely from this depreciation in the dollar, not from the investment's performance.

In other words, returns reflected both strong international market performance and a weakening dollar, which amplified these gains when translated back into dollars.

Source: ICE Data Indices (U.S. Dollar Index) and central bank exchange-rate data, via YCharts. Data reflects percentage change from 1/1/2025 through 12/30/2025. Currency movements are shown for illustrative purposes only and do not represent investable returns.

Currency effects can meaningfully boost returns in the short term, even if the underlying local market performance is more modest. At the same time, investors became more cautious amid concerns around government spending, tariffs, and broader economic uncertainty. As investors became more risk-averse, capital started to shift away from U.S. assets toward alternatives, including international markets and more defensive assets, such as gold.

Together, a weaker dollar and shifting investor sentiment helped lift international markets, even before considering the vast policy changes.

Government policy has also played a meaningful role in recent market performance.

Several overseas economies have leaned on fiscal spending, incentives, and support programs to stabilize growth. These measures can lift markets in the near term, but they often move faster than underlying economic fundamentals.

- China has indicated continued fiscal support for 2026, alongside an emphasis on technological self-reliance. Markets have responded positively, though long-term outcomes remain uncertain.

- Japan has committed to more proactive spending after decades of limited economic growth, which is helping to improve investor confidence.

- Europe has increased its spending on defense and infrastructure amid geopolitical pressures, which is expected to support economic activity in the near term.

- Brazil and Mexico have relied on more targeted measures, such as tax adjustments and investment incentives, which have provided a temporary uplift.

These actions help explain why international markets have looked particularly strong. Government support can be practical, but it is not the same as organic, sustainable growth.

Recent international outperformance has been mainly driven by currency movements, shifts in investor sentiment, and policy support, rather than a sudden change in long-term fundamentals. These forces can lift markets for a short time, but they can also reverse just as quickly. Periods like this serve as an important reminder:

A globally diversified portfolio is designed to work quietly and consistently,

not just when headlines make it feel important.

~ Ricardo Salinas

The opinions expressed are for general informational purposes only and are not intended to provide specific investment advice or recommendations for any individual. To determine which investments may be appropriate for you, consult your financial advisor prior to investing.

All performance referenced is historical and is not indicative of future results. Market conditions are subject to change. Indices are unmanaged and cannot be invested into directly. Index performance does not reflect the deduction of advisory fees, transaction costs, or taxes.

Investing involves risk, including the potential loss of principal. Diversification and asset allocation strategies do not guarantee profits or protect against losses in declining markets. International and emerging market investing involves additional risks, including currency fluctuations and political and economic instability, and may not be suitable for all investors.