Houston, We Have an IPO

Advisors' phones have been busier than ever. Emails before coffee. Texts after dinner. And every one of them seems to be asking the same thing, “Should I buy the SpaceX IPO?”

This is a fair question, given that it’s one of the most talked-about and widely popular IPOs in a generation, brought to the market by one of the most prominent and widely covered entrepreneurs of our time, Elon Musk. So, let’s talk about it.

I’m not going to tell you whether you should buy it or not. That’s not what this is. What this is, is me making sure you fully understand what you’re really looking into before doing anything.

SpaceX just filed its IPO paperwork (also known as an S-1) with the SEC on May 20th. The document runs about 200 pages, of which roughly 40 are devoted to rockets and satellites (pretty cool looking), and 30 are dedicated solely to risk disclosures. I read it. Here are the most important things that stood out to me.

Rocket Company? Are you sure about that?

When people first hear the company SpaceX, they think of rockets. Which is completely understandable, considering the company's official name is “Space Exploration Technologies Corporation”.

But the company going public isn’t JUST a rocket company. The company is split up into three differentiated business segments.

The first is the launch of rockets, including Falcon 9 and Starship. This is where the brand has been built. However, it is currently operating at a loss, largely because SpaceX has had to devote $15 billion to developing Starship, its next-generation rocket. Cool but expensive.

The second is Starlink. SpaceX’s satellite internet service. The real engine of the company. Starlink has over 10 million paying subscribers across 160 countries. This is the only business segment that is profitable today. The other two segments are essentially running up Starlink’s tab.

The third is AI. In February of this year, SpaceX merged with Elon Musk’s AI company, xAi, which also owns X, formerly known as Twitter. Although profitability wasn’t his biggest concern during this acquisition, this segment is early, expensive, and generating losses at a significant rate.

Three businesses. One stock. All at different stages.

The Fun Stuff. Financials.

SpaceX brought in $18.7 billion in total revenue in 2025, according to the S-1. This sounds impressive until you realize the company actually posted a GAAP (Generally Accepted Accounting Principles) net loss of $4.9 billion for the same year.

Here’s why, in layman’s terms.

Starlink is profitable by a wide margin. The rocket business and the AI business are not. However, it is important to differentiate why and how. The AI segment lost $6.35 billion last year alone, mainly due to infrastructure investments. Tipping the whole company into the red. On top of that, SpaceX pays much of its top talent in company stock rather than cash, and, under accounting rules, that is recorded as an expense. Lastly, the Starlink satellite constellation depreciates over time, resulting in ongoing charges, even though the money has already been spent.

Think of it like this: Starlink is currently the company's only profitable segment, generating the cash flow needed to support the other segments. The rest of the company is a bet on the future. Whether this plays out is the bet investors are being asked to make.

The Excitement is Granted

The excitement around the IPO isn’t irrational. It is worth saying that.

SpaceX was founded in 2002 with a mission to make humanity multiplanetary. Although this may sound like a reach, along the way, Elon has changed the economics of space travel, built the world’s largest satellite internet network, and delivered Wi-Fi connectivity to communities that have never had reliable access. These are real, documented achievements, not just press releases.

The mission statement is what investors have to believe they’re paying for. Not today’s financials. The version of this company that they believe will exist in a decade from now.

What Public Shareholders Actually Own

This part is worth taking a few minutes to read over, as it often gets lost in the excitement.

The S-1 states that SpaceX uses a dual-class share structure. What does this mean? Elon holds Class B shares, which carry 10 votes each. The public can only buy Class A shares, which carry one vote each. The S-1 confirms that Elon will retain 85% of the combined voting power after the IPO.

In plain English, public shareholders will be able to have an economic stake in the company's results, upside and downside, while having no meaningful say in how the company is run. Musk will manage all decisions when it comes to business strategy, leadership, and direction. The S-1 explicitly states that SpaceX will be a “controlled company” (with one shareholder holding more than 50% of voting power) under Nasdaq’s governance rules.

This is not my opinion or my criticism. It is stated in the filing, and it is important to know.

Why IPOs Are Historically Volatile

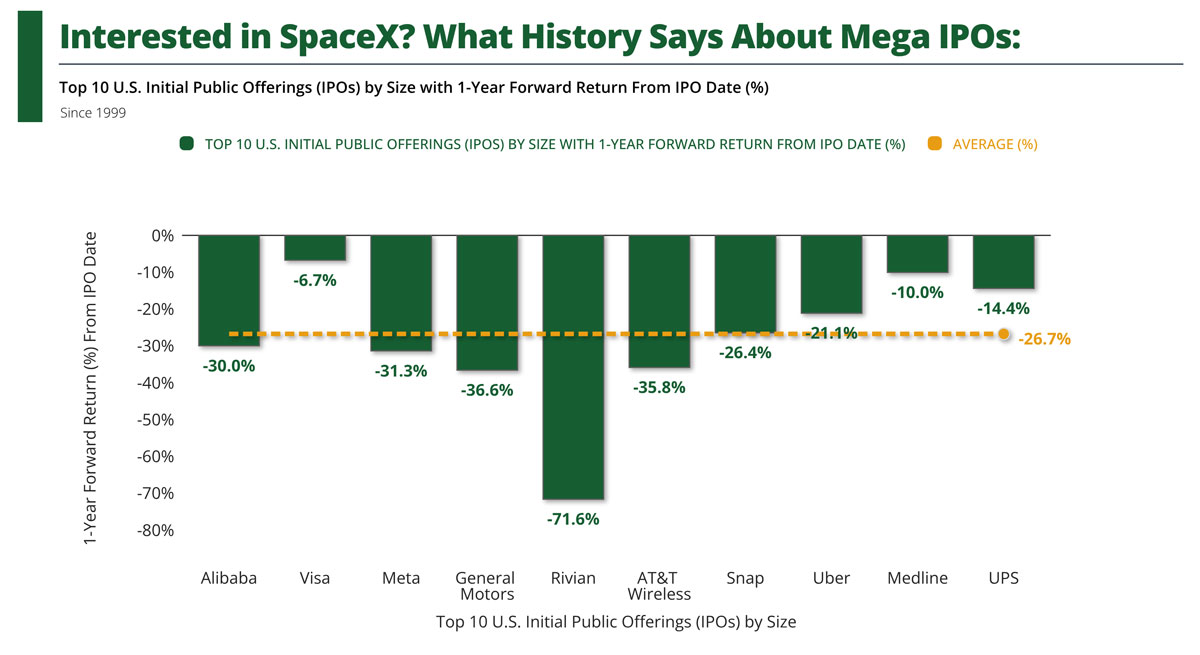

Here’s something that often gets left off the highlight reel on opening day. The buzz and hype around an IPO and actual returns are two very different things. Jay Ritter, a professor at the University of Florida who has spent the past few decades studying IPOs, has tracked a consistent pattern over the past 40 years. His data shows that, across more than 1,500 IPOs from 2012 to 2024, the average newly public company underperformed the broader market (S&P 500) by more than 25% in the three years following its listing. The chart below tells a similar story: among the 10 largest IPO’s since 1999, the average one-year return is about -26.7%. Once the excitement begins to fade, the real work of growing into the valuation begins.

Source: © Exhibit A, FactSet Research Systems Inc., Standard & Poor's | Latest: 2026-05-29

There is also a lock-up period that is rarely talked about.

Insiders, including employees, early investors, and executives, are typically prohibited from selling shares for a set period following an IPO. In SpaceX's case, the S-1 discloses a staggered structure rather than a single unlock at 180 days. Insiders will have several windows to sell shares between Q2 earnings and mid-December, with the first gate opening after Q2 results. The full lockup expires around mid-December 2026. Whether staggered or not, when these windows open, selling pressure may follow.

Importantly, I'm not predicting this IPO will have the same fate, just stating the historical pattern.

None of this means SpaceX isn’t a sound long-term investment. Some of the most valuable companies in the world today rewarded patient investors who bought and held on the IPO date. But, not to shy away from the fact that the first year of trading is historically a bumpy ride.

The Questions You Should Be Asking

Does this fit where you are in life currently? Are you comfortable holding through volatility if it shows up? And most importantly, are you drawn to this because it fits your specific plan or because everyone is talking about it?

These aren’t meant to be rhetorical questions. They’re questions that truly matter.

If you want to talk it through, as always, feel free to reach out.

~ Ricardo Salinas

This post is for informational and educational purposes only and does not constitute a recommendation to buy, sell, or hold any security.

All financial data, business descriptions, subscriber figures, segment results, governance disclosures, and ownership structure referenced in this post are sourced from SpaceX's preliminary Form S-1 registration statement filed with the U.S. Securities and Exchange Commission on May 20, 2026. The xAI merger referenced in this post is sourced from SpaceX's official company update, available at spacex.com/updates.

IPO long-run performance data is sourced from "Initial Public Offerings: Updated Long-run Statistics" by Jay R. Ritter, Emeritus Professor of Finance and Director of the IPO Initiative, University of Florida Warrington College of Business, updated March 23, 2026, available at site.warrington.ufl.edu/ritter/files/IPOs-long-run-returns-on-IPOs.pdf, Table 11a. This is a third-party source provided for general educational context only and does not constitute a prediction of SpaceX's future performance.

Third-party information contained herein is obtained from sources believed to be reliable; however, KWB Wealth does not independently verify and cannot guarantee the accuracy or completeness of such information.

KWB Wealth is not affiliated with SpaceX, Starlink, xAI, X, Nasdaq, FactSet Research Systems Inc., Standard & Poor's, or the University of Florida.

Past performance is not indicative of future results. Investing involves risk, including the possible loss of principal. Please consult your KWB Wealth advisor before making any investment decisions.